Industrial insurance is often still considered the insurance industry’s Champions League. However, German and European insurance and brokerage companies in this field are lagging far behind the possibilities when it comes to digitalization and still work far too much manually. The private insurance industry is much further along in this respect. Certain industries, lines of business and products are also very well suited to drive digitalization in the industrial insurance sector and thus bring more efficiency to processes.

Short & Concise

- Private insurers are further ahead than industrial insurers

- Standard: Complexity as a barrier to digitisation

- Players must reduce fear of contact and leave silos

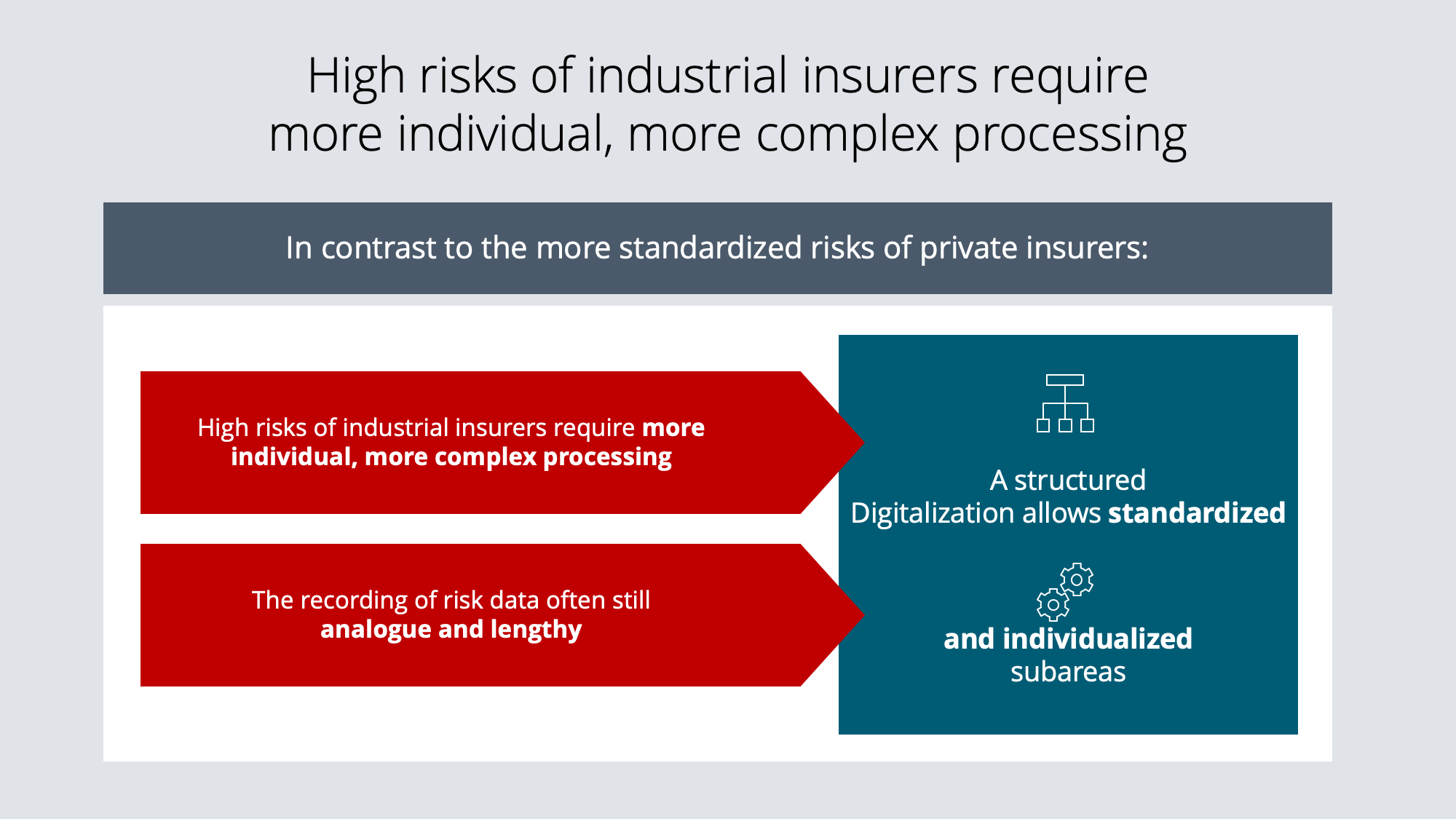

As things stand at present, there are no standardized processes for the industrial insurance sector that would be a prerequisite for the digital networking of the players among themselves. The recording of risk data and their distribution to several industrial insurers, possibly even by invitation to tender, still takes place in analogue form and – to the dissatisfaction of customers – takes far too long. It is also difficult to explain to customers and brokers why other lines of business have been digitalized and why the tendering process is still handled manually in industrial insurance.

In part, this lagging behind the private insurance industry is due to the special risks in the industrial insurance sector. The greater the risk and the larger the insurance volume, the more individual the risk assessment must be. On the other hand, there is a deep-rooted thinking in the industry that something as complex as industrial insurance cannot be digitized at all. However, this does not apply to products and lines of business that cover standardized risks and companies with sales of less than one hundred million euros.

An ideal introduction to the digitalization of industrial insurance: Small and medium-sized enterprises

It would be particularly important and sensible to drive digitalization forward in small and medium-sized businesses and in trade and industry with two to three digit numbers of employees and a sales volume in the double-digit million range. In this area, the effort of individual risk assessments is hardly worthwhile for insurers. This is where the digitalization of the industrial insurance industry can begin most effectively.

There are also some of the divisions and products that could make digitalization more easily than others. These include first and foremost financial lines, such as D&O, E&O and Cyber. In a next step, innovative and individual products specialized for specific target groups can be digitized.

Structuring preparatory work more difficult than implementation

How do you get there? The technical implementation with a software or for example with a platform is only the last and perhaps less complicated step. In advance, processes and products that were previously highly individual must be standardized and structured so that they fit into grids, categories, schemes and digital tariffs. To do this, threshold values must be defined, wordings assigned, sets of rules created and, in some cases, decisions simplified.

Key success factor: communication

Important for the success of the project in the industrial insurance sector: insurers and brokers must talk to each other and overcome any fear of contact. A digital platform that could be created in this way would have to be fair, transparent, independent and useful for all parties involved, i.e. for insurers, brokers and, above all, customers. The ideal platform does not depend on a central operator who has control over processes and data, but integrates all players on an equal footing.

The willingness for such an approach seems to be increasing at the moment compared to previous years. It is likely to be several years before such a platform is really ready for use, and it is likely that over time several platforms serving different market segments will be established. Cost pressure will contribute to acceleration.

Conclusion

The industrial insurance sector is lagging behind the private customer sector in terms of digitalization. This has to do with individual risks and offers that are difficult to standardize. To close this gap, all relevant players must work together. In order for investments in new platforms to pay off, the SME market is an attractive segment due to its larger volumes. The cost pressure in the industry will lead to visible results in the next few years, as digitalization means increased efficiency and thus profits.

Photocredit: gmast3r / iStockphoto