Online marketplaces have the potential to revolutionize the customer interface in industrial and commercial insurance for small and midrange businesses (SMBs). The preconditions for insurers to set up a platform together are better today than ever before.

In this first part of the series we explain why the outlook for establishing a marketplace that enjoys industry-wide acceptance is currently so good. In the second part we take an initial look at the steps required to establish it and consider what an insurance marketplace might look like.

Marketplaces are considered to be the Mecca of online business. Customers set out on a pilgrimage to the established Internet sites to gain bundled access to what different suppliers offer. In 2016 over 50 percent of product searches in the United States were launched on Amazon and not on Google.[1]

The focus is on the customer. He or she consults the Web and the Web provides answers.

The success of marketplaces is a direct consequence of digitization. Classical business via middlemen used to be the de facto standard. Today direct sales and marketplace business are thriving on the Internet. In both cases the central principle of online distribution – that the focus is on the customer – applies. He or she consults the Web and the Web provides answers.

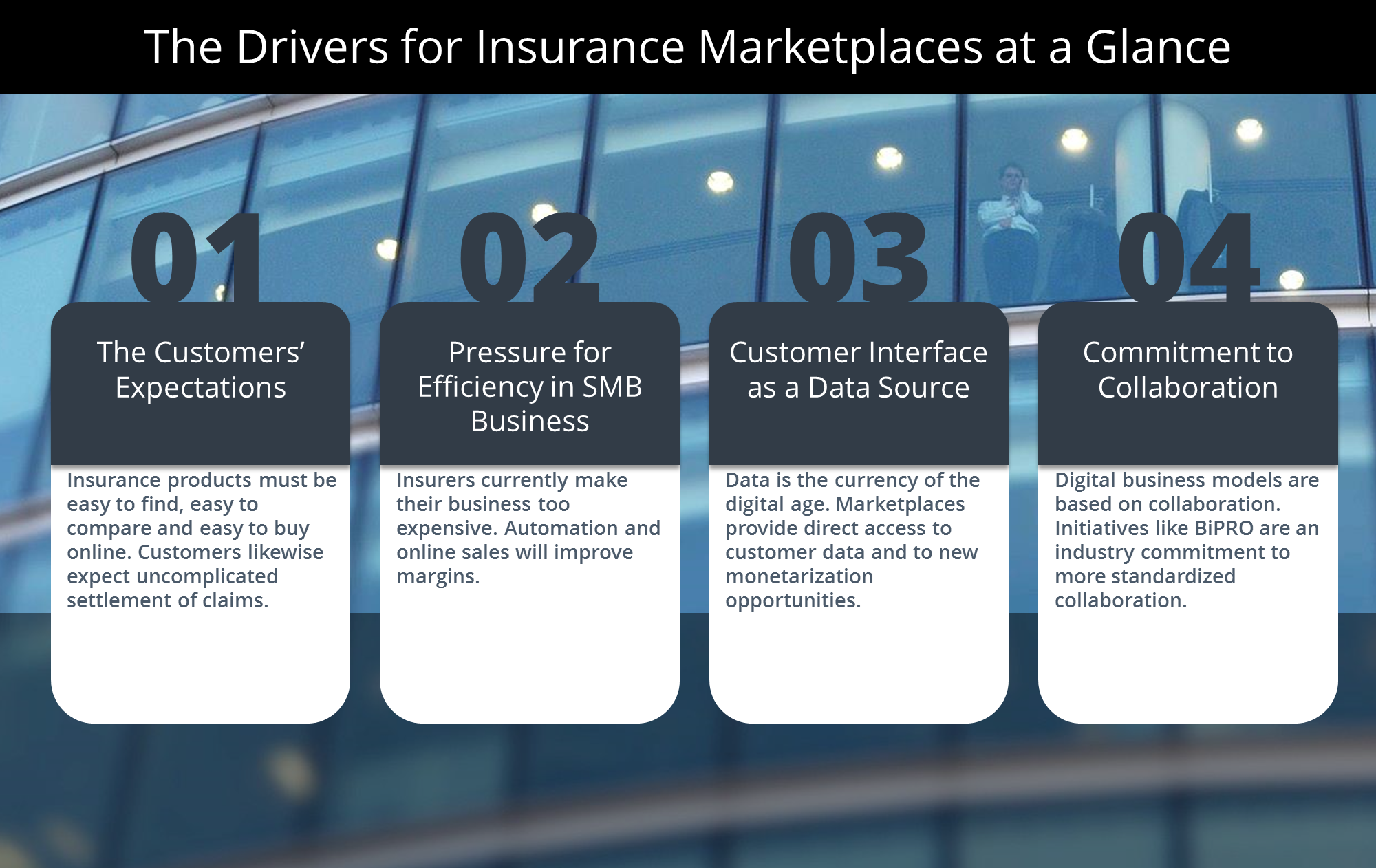

There is a strong likelihood that online marketplaces will prevail in industrial and commercial insurance too, and SMB business fulfills the fundamental prerequisites. There are standardized products and a substantial demand for comfort, or ease of use. Low premiums and attractive loss ratios suggest extensive automation of sales processes.

At the same time customers are increasingly prepared to purchase more complex products on the Internet. Taking out insurance cover online is no longer an exotic scenario. What remains to be seen, however, is who will succeed in setting up a marketplace that enjoys industry-wide acceptance.

Catalytic Effect of the Digitization Concept

The best prospect of establishing an online marketplace for industrial insurance is that of a joint venture set up by insurers.

The best prospect of establishing an online marketplace for industrial insurance is in our opinion that of a joint venture set up by insurers themselves, and not by brokers or InsurTechs. For one, insurers are under pressure to act. There will only be one Amazon of the industrial insurance business. For another, they are well positioned. For years they have tended step by step to go for a gradual digital evolution rather than a sudden, uncontrolled revolution – with results that can be seen both in underwriting and in digital processing of claims.

Insurers have thereby made a great deal of progress outside of the media limelight. In sales the trend began with the provision of Web services for sharing tariffs. That makes commercial insurers compatible online. Standardization is also making significant progress. The BiPRO standards that have been drawn up and are planned, for example, testify to a strong commitment on the industry’s part. They are a clear undertaking to collaborate in a more standardized way.

Digitization has likewise made headway in claims, driven by the need to improve loss ratios, with insurers setting up new capabilities for automated loss classification based on predictive models and subsequent claims processing. For a marketplace this capability will clearly play a key role in ensuring customer satisfaction and acceptance.

Unlike InsurTechs insurers have, along with the capital resources, the customer base and the brand strength required to establish a platform.

Further reasons why the time is ripe for establishing a common industry-wide marketplace are that digitization is itself high on the agenda of all market participants, leading to substantial investments, and unlike InsurTechs insurers have, along with the capital resources, the customer base and the brand strength required to establish a platform. In addition to setup costs investment in ongoing development of the marketplace offering is required. Setting up a marketplace that is accessible for all market offerings would enhance these opportunities exponentially.

Those who Hold the Data Control the Digital Business

Marketplace operators have control over the customer interface and direct access to customer data. That is one of the reasons why marketplaces are so attractive for insurers. Data is seen as the currency of the digital age and the battle for SMB customer data between insurers and brokers has long been in full swing.

The overriding objective of all market participants in the SMB sector is to make the business fully automatic – from the tender via the definition of cover offered to loss adjustment. Despite its enormous potential SMB business is currently very cost-intensive due to long in-house processing times and too much manual input in spite of standardized products.

At present, brokers control the customer interface. In order to map the entire process chain digitally they are moving into typical areas of insurers’ work, such as by setting up Managing General Agents (MGAs) who in addition to classical brokerage act as insurers without capital.

A neutral marketplace will occupy a key position in controlling the customer interface.

From the insurers’ perspective, policies sold via brokers and other sales organizations are a relic of the “old world.” As a result of digitization, process costs of interaction with customers are reduced. Digital consulting services and automated comparison facilities could soon make intermediaries for SMB products superfluous. By joining forces insurers will ensure a product variety that only large brokers are now able to offer. A neutral marketplace will occupy a key position in controlling the customer interface.

[1] bloomreach: State of Amazon 2016 – http://go.bloomreach.com/rs/243-XLW-551/images/state-of-amazon-2016-report.pdf